Doing Business in Chile 2026

Editor’s note

Chile: A dynamic market at a pivotal moment

Based in Santiago, I have been covering Latin American markets for several years — advising on regional market strategy and tracking business and political developments across the region. Although all Latin American countries present opportunities, Chile stands out as a potential key market for the decades to come.

With the largest copper reserves on earth and the world’s most advanced lithium governance framework, massive recent investment in solar and wind energy, an emerging green hydrogen and ammonia industry, new desalination plants and data centres — Chile is positioning itself as one of the drivers of the global energy transition. The combined development of its mining, energy and technology sectors, through innovation, environment-friendly policies and openness to global markets, makes Chile a truly singular and dynamic market.

The country’s strength also lies in its capacity to adapt quickly and efficiently to change. Companies operate across an extraordinary range of environments — from the hyperarid Atacama to the glaciers of Magallanes — each requiring distinct engineering and operational responses. This adaptability extends to technology: Chile is at the forefront of the digital revolution in Latin America, leading the region in internet coverage, data centre infrastructure and AI adoption. In some international rankings it outperforms several Western economies. Santiago is also rapidly transforming its urban mobility model, with new metro lines under construction, a pioneering cable car network and one of the world’s largest electric bus fleets — a model that other Chilean cities are beginning to replicate.

Chile also went through a turbulent period between 2019 and 2022, marked by social unrest and two failed constitutional revision processes. That page appears to have been turned — and decisively so with the December 2025 election of José Antonio Kast, arguably the most significant political shift the country has seen since its return to democracy. The new president brings a pro-business agenda: lowering corporate taxes, cutting permitting delays for environmental licences and trimming government spending.

This ambition will not be easy to translate into policy. The Kast administration controls neither the Senate nor the Constitutional Court, and tensions may arise both within the governing coalition and from civil society if budget cuts deepen or environmental commitments are perceived to weaken. Investors should treat the promised reforms as upside optionality rather than base-case assumptions — the “Risks & Points of Vigilance” section of this report addresses these dynamics in detail.

This Country Profile is designed to provide a structured, data-grounded starting point for that engagement — not to replace the due diligence and local relationships that any serious commitment to Chile requires. I hope it proves a useful foundation.

Economic Overview

Chile is one of Latin America’s most open, stable and dynamic economies. Backed by strong institutions, disciplined fiscal policy and an outward-oriented trade strategy, the country offers a reliable and predictable environment for foreign investors and exporters. With one of the highest GDP per capita figures in the region, a modern financial system and a legal framework that protects property rights, Chile consistently ranks among the top destinations for foreign direct investment in Latin America. Located between the Andes and the Pacific Ocean, Chile stretches over 4,000 km from the Atacama Desert to Patagonia — a geography that underpins exceptional diversity in mining, agriculture and renewable energy. Its membership in the OECD, the Pacific Alliance and more than 30 free trade agreements covering over 60 countries (representing roughly 88% of global GDP) makes Chile a strategic hub for regional market access.

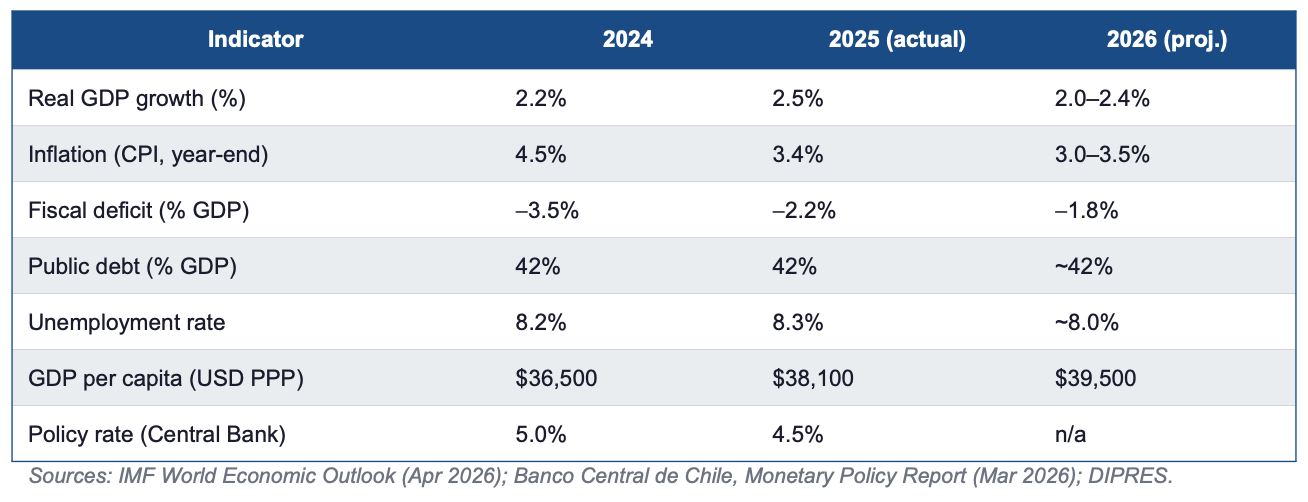

Key Macroeconomic indicators

Chile’s economy grew 2.5% in 2025 — in line with IMF forecasts and consistent with its estimated potential growth rate. Growth was led by private consumption, driven by continued real wage gains, and mining and energy investment. The Central Bank completed a rate-cutting cycle through 2025, bringing the policy rate to 4.5% by December, though the Middle East conflict and higher oil prices introduced fresh inflationary uncertainty in early 2026. For 2026, the IMF projects GDP growth of 2.0–2.4%, with the central bank’s own range standing at 1.5–2.5%. Fiscal consolidation has advanced: the fiscal deficit narrowed from 3.5% of GDP in 2024 to 2.2% in 2025, supported by reduced expenditure and a revenue rebound. Chile holds a stable sovereign credit rating (Moody’s: A2; S&P: A−), reflecting sustained investor confidence in its institutional framework.

Political Environment: A New Administration

José Antonio Kast of the Republican Party won the presidential runoff on 14 December 2025 with 58.2% of the vote, defeating Jeannette Jara of the Communist Party. Kast took office on 11 March 2026, marking Chile’s most significant political shift since its return to democracy in 1990. The election was primarily driven by public concerns over rising organised crime and irregular migration, rather than traditional economic divisions.

On the economy, Kast has committed to reducing public spending by USD 6 billion over 18 months, lowering the corporate income tax rate from 27% to 23%, and deregulating key sectors. His administration is expected to accelerate mining and energy permitting, building on the Ley de Permisología (Law 21.770) enacted in September 2025, which creates a single digital portal for permits and introduces simplified procedures for lower-risk projects. Analysts anticipate pragmatic conservatism: incremental tax and regulatory reform rather than sweeping austerity, given the need for cross-party support in a Congress where the right holds a majority but not a supermajority. Chile remains a consolidated democracy with respected institutions, an independent judiciary and transparent public procurement. The country ranked 27th globally on Transparency International’s Corruption Perceptions Index in 2023, the strongest score in Latin America.

Key Sectors & Business Opportunities

Mining & Critical Minerals Chile is a cornerstone of global critical mineral supply. It holds approximately 23% of the world’s known copper reserves and supplies around 28% of global copper production — some 5.5 million tonnes per year. The northern Atacama region concentrates this wealth, with flagship operations including Escondida (the world’s largest copper mine), Collahuasi and Chuquicamata. Cochilco projects Chilean copper output to reach 5.6 million tonnes in 2026 and 5.9 million tonnes in 2027, supported by a $105 billion sector investment pipeline through 2034. Copper prices averaged…

To access the full Chile Country Profile in PDF format, subscribe for free to Latinsight’s newsletter.