Latin America’s Slow Growth Problem

Latin America is growing. It has been growing for four consecutive years — and yet the region is falling further behind. At roughly 2% annually, growth barely keeps pace with population increase, generates insufficient formal employment, and lags well behind other emerging market regions in productivity gains. The region has achieved stability but can it translate it into structural transformation?

According to the ECLAC, the region is stuck in a “low capacity for growth” trap

A regional low growth trap

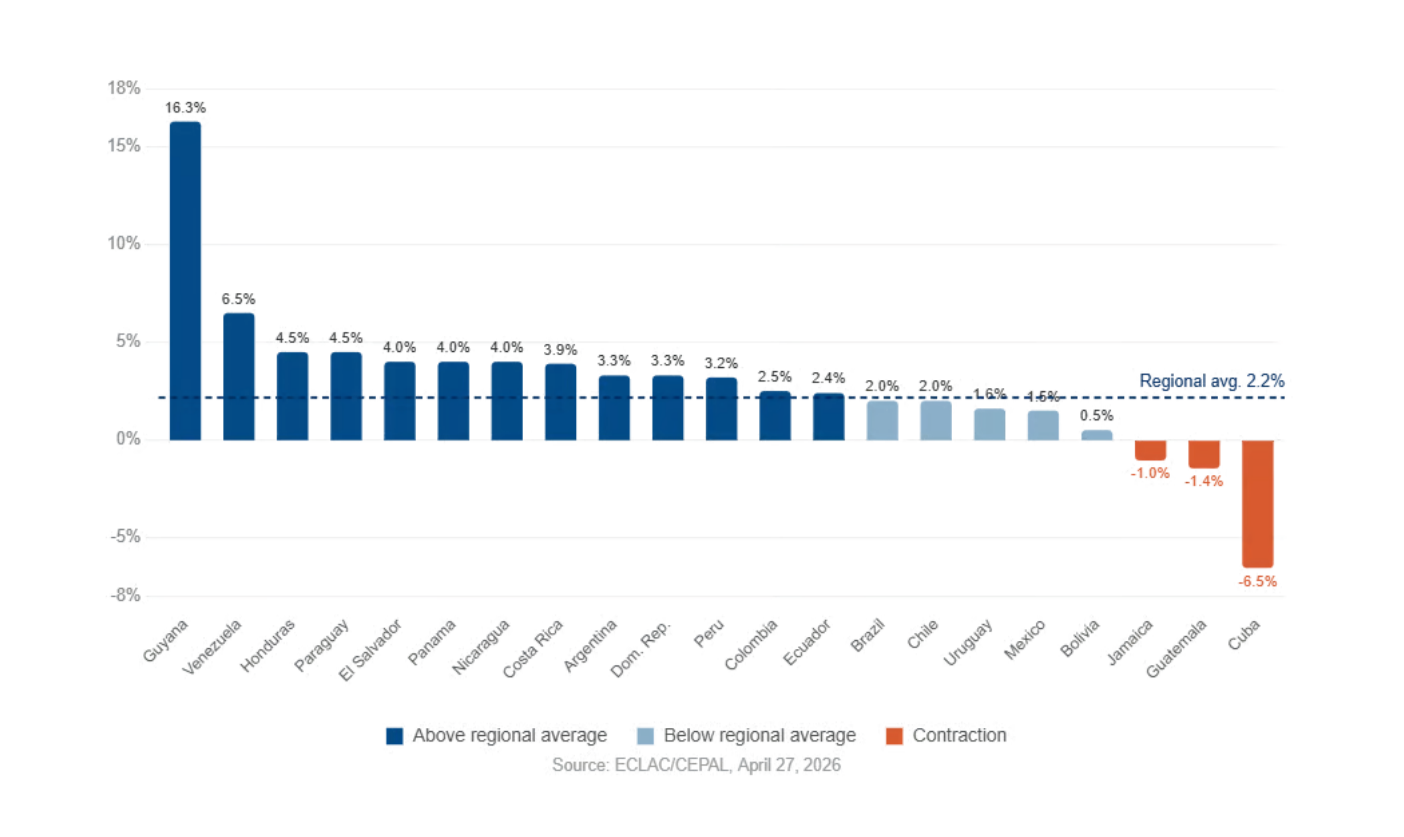

Latin America and the Caribbean is projected to grow 2.2% in 2026, a slight downward revision from the 2.3% estimated in December 2025. Growth will decelerate in 24 of the region's 33 countries, and accelerate in just seven. If this projection holds, the region will have registered four consecutive years of growth rates around 2.3% — a pattern that ECLAC explicitly describes as a "low capacity for growth" trap.

2026 GDP growth projections for Latin America and the Caribbean - ECLAC, April 27 2026

The World Bank's assessment is consistent: it projects regional GDP growth at 2.1% in 2026, below the 2.4% recorded in 2025, with investment remaining weak amid high global interest rates, slowing growth in advanced economies and China, and trade policy uncertainty.

The external environment is not helping. The average oil price in the first three weeks of April was 74% higher than in December 2025, generating inflationary pressure and raising production and transportation costs across the region. The WTO forecasts global trade volume growth of only 2.7% in 2026, down from 4.7% in 2025, compressing the external demand on which many regional exporters depend. At 2% annual growth, Latin America is barely keeping pace with population growth, generating insufficient formal employment, and falling further behind other emerging market regions in productivity and income convergence.

The aggregate figure conceals a wide dispersion. Nine countries are expected to grow at 4% or more — Paraguay, Honduras, El Salvador, Panama among them — while three face outright contractions, including Cuba (-6.5%) and Guatemala (-1.4%). The English and Dutch-speaking Caribbean is projected to grow 5.6%, largely on the back of Guyana's oil boom; excluding Guyana, the Caribbean average drops to 1.2%. The structural winners share a common profile: commodity exporters with credible macro frameworks, low public debt, and exposure to sectors benefiting from the Iran conflict price surge — oil, copper, lithium, agricultural commodities. The structural losers are energy importers with limited fiscal space and high dependence on US demand — primarily Central American economies and parts of the Caribbean.

Paraguay: South America's quiet outperformer

Paraguay illustrates what escaping the trap looks like in practice. The country is projected to grow above 4% in 2026 — the strongest performance in South America after Guyana's oil boom and Venezuela — after expanding 6.6% in 2025, more than double the regional average. The World Bank and IMF attribute this to two decades of disciplined macroeconomic management: inflation at 3.1% in 2025, public debt among the lowest in the region, and a fiscal deficit reduced to 2% of GDP. S&P and Moody's have both awarded investment grade in the past two years, unlocking a new wave of foreign capital.

The growth drivers are diversifying: beyond soybeans, construction and services are accelerating on the back of capital inflows from neighbouring countries seeking lower tax burdens. Brazilian firms relocating manufacturing operations are a notable example. Cheap hydroelectric power from the Itaipú and Yacyretá dams gives Paraguayan industry a structural cost advantage that is increasingly attracting green industry investment.

Three structural risks persist: the need for large-scale public-private infrastructure projects above $1 billion, pending fiscal reforms to address a pension system deficit, and a judiciary that analysts flag as requiring institutional strengthening. Paraguay's story is real but it remains a small, commodity-exposed economy in a volatile global environment.

Subscribe to Latinsight publications for free and access a EU-Mercosur Business Opportunity Guide

The fiscal constraint

ECLAC's Fiscal Panorama 2026, presented on May 6, adds a further layer of difficulty: public debt in Latin America reached 52.3% of GDP in 2025, up from 51.9% in 2024, remaining near the levels of the early 2000s when the region confronted a series of financial crises. The region continues to operate with limited fiscal space in a context of higher financing costs. CEPAL's Executive Secretary framed the challenge directly:

"The region is mired in three development traps: one of low capacity for growth and transformation; another of high inequality, low social mobility and weak social cohesion; and a third trap of low institutional capacity and weak governance. These traps are not isolated from the external environment. On the contrary, international shocks deepen them and make them harder to overcome. And that is precisely where fiscal policy must play a central role: as a stabilization mechanism against external shocks, and as a strategic tool for driving development"

José Manuel Salazar-Xirinachs - ECLAC’s Executive Secretary

The Fiscal Panorama calls for closing personal income tax compliance gaps estimated at 0.33–0.93% of GDP and improving the transparency and effectiveness of tax expenditures — neither of which translate into quick fiscal space, but both of which are preconditions for the sustained public investment the region needs. The challenge is structural: governments facing election cycles have limited political appetite for tax reform, and those with the lowest institutional capacity are precisely those that need it most.

The industrial policy debate

Into this constrained environment enters a significant intellectual shift. The World Bank's March 2026 report "Industrial Policy for Development" marks a formal reversal of the institution's longstanding scepticism toward state-directed economic strategy. The argument, defended pointedly by chief economist Indermit Gill in The Economist, is not that markets are wrong but that the facts changed: GDP per capita has doubled since 1993, schooling levels have risen, and macroeconomic management has improved in most countries. More governments now meet the prerequisites for industrial policy to work.

For Latin America specifically, the Bank's prescription is precise. The region should abandon traditional import substitution in favour of a "learning policy" approach — building capabilities, facilitating experimentation, and exploiting openness rather than protecting incumbents.

The Bank explicitly flags Argentina's Tierra del Fuego regime as a cautionary example: decades of protection without measurable productivity gains. Priority areas are digital connectivity, green industry investment, STEM human capital, and management quality. The instrument of choice is horizontal — skills, infrastructure, institutions — rather than vertical subsidies to specific sectors or firms. The region’s structural challenge is a significant one: a massive informal sector with limited ambition to scale coexists with a small pool of high-performing firms, while scarce skilled labour and shallow financial markets act as binding constraints on any industrial strategy regardless of its design.

🎯 Strategic perspective

The 2% growth forecast is a structural constraint, not a crisis. Aggregate demand across most markets will remain subdued, fiscal space for public investment will stay limited, and monetary easing will be slower than initially anticipated. The selective opportunities lie in the countries growing above trend, in commodity sectors benefiting from elevated global prices, and in the companies positioned to supply the skills, technology, and logistics infrastructure that industrial policy ambitions will require.

No country seems to offer a replicable model for the region. However two countries stand out for different reasons: Paraguay demonstrates that disciplined macro management, low taxes, and a stable institutional framework can sustain above-average growth over decades, even in a small commodity-exposed economy. Uruguay, often overlooked in regional debates, offers a more complete picture: it combines investment-grade sovereign debt, a functioning social contract, relatively strong institutions, and a track record of horizontal industrial policy in areas like software exports and renewable energy.

Neither is a template that larger, more complex economies can copy wholesale — but both demonstrate that the prerequisites the World Bank and ECLAC identify are achievable in the region, and that the returns are real.