Understanding Bolivia's Crisis

Bolivia is in the midst of a significant social crisis that is a convergence of three distinct pressures: a decade-long structural deterioration of hydrocarbon revenues, a reform programme that has accelerated the cost of adjustment, and the lasting influence of former President Evo Morales over the country's politics. Understanding the three together is essential for any assessment of what happens next.

Supporters of Evo Morales march toward downtown La Paz to demand the resignation of President Rodrigo Paz after 16 days of blockades. REUTERS/Claudia Morales

Recent developments

The protests began in early May, initially triggered by a law designed to allow land mortgages, a major shift for Bolivia’s agricultural sector. Faced with criticism, President Paz annulled the law on May 13, but the demonstrations did not stop — they expanded. Miners, teachers, transport workers, farmers and indigenous groups joined, each with distinct but overlapping demands: wage increases, the maintenance of fuel subsidies, and labour reform. Over 16 days,road blockades stranded around 5,000 truckson key highways, leaving supermarket shelves empty and hospitals without medical supplies in La Paz and other cities. Argentina launched a humanitarian airlift at Bolivia's request.

On May 16,security forces deployed 3,500 police and soldiers to break the blockades. On May 18, thousands of protesters — including Morales supporters who had marched seven days from Caracollo in Oruro — converged on La Paz, attempting to storm the Plaza de Armas and the Government Palace. Police responded with tear gas over several hours, and at least two protesters were reported injured. A group of demonstrators looted a national property registry office. The public prosecutor ordered the arrest of Mario Argollo, leader of the COB — Bolivia's main labour union — on charges of public incitement and terrorism, a move likely to escalate tensions further rather than contain them.

The context: a deep structural economic crisis

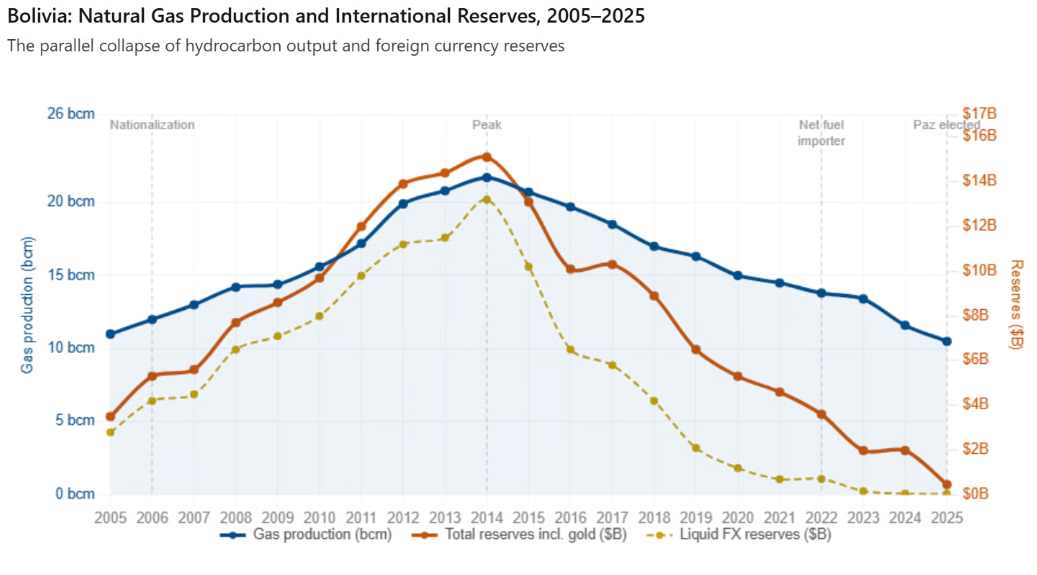

Bolivia's current crisis has its roots in a commodity boom that ended a decade ago and was never replaced. Natural gas production peaked at 21.7 billion cubic meters (bcm) in 2014 (over $6 billion in annual export revenues) before entering a prolonged structural decline driven by chronic underinvestment in exploration. By 2024, production had fallen to 11.6 bcm, generating just $1.1 billion in export revenues.

The mechanism behind this collapse is well-documented: the 2006 nationalisation of the hydrocarbon sector under Morales raised taxation to the point where foreign operators either exited or halted exploration spending, leaving the state company YPFB, never designed as an exploration entity, responsible for a task it was institutionally and financially ill-equipped to perform. Reserves were drawn down without being replenished. Bolivia became a net fuel importer in April 2022. This structural shift has no near-term reversal in sight, given that Bolivia's gas contract with Brazil expires this year and Argentina, once a second major customer, has achieved self-sufficiency through Vaca Muerta.

The fiscal consequences were compounding. During the boom years, the MAS government built a social model — subsidised fuel, food transfers, infrastructure investment — financed almost entirely by hydrocarbon revenues channelled through YPFB and the state budget. As revenues declined, the government maintained expenditure by drawing down reserves and, increasingly, by financing the deficit through central bank money creation. After a peak at $15.1 billion in 2014 (equivalent to roughly 51% of GDP), international reserves fell to $1.98 billion by end-2024, of which $1.89 billion were in gold held at the legal minimum. Liquid foreign exchange reserves — the dollars actually available for import payments and debt service — collapsed to $47 million by December 2024, a figure that barely covers two days of imports. The parallel black market exchange rate has reached a 40-70% premium over the official rate, creating severe distortions in trade pricing and contract enforcement.

The macroeconomic consequences are now fully visible as Bolivia's GDP contracted 1.58% in 2025according to the National Statistics Institute. It is the first full-year contraction in four decades. The IMF projects a further contraction of 3.3% in 2026. The government's own reformulated 2026 budget projects a 9% fiscal deficit and 14% annual inflation — down from a peak of 25% in mid-2025, but still among the highest in the region. The conflict in the Middle East has added external pressure: higher global oil prices have increased the cost of fuel imports that Bolivia can barely afford, compounding the domestic shortage that is now a direct trigger of the protests.

The reform agenda and its limits

Rodrigo Paz was elected in October 2025 as Bolivia's first centre-right president since 2006, inheriting what his own officials described as the most severe economic crisis in forty years. His early measures were credible: over $8 billion in multilateral financingsecured from IDB, CAF and JICA, a double-notch S&P upgrade to CCC+, and a $388 million bond payment met in March. He eliminated fuel subsidies — a structural necessity given the fiscal deficit — while preserving social welfare programmes and adding new benefits for informal workers.

The difficulty is well-documented in the fiscal reform literature: adjustment measures generate social costs immediately, while their macroeconomic benefits materialise over years. Paz's victory over more right-wing candidates also signalled the electorate's unwillingness to support drastic austerity — a mandate for reform, but not a blank cheque for shock therapy. With $47 million in liquid reserves and 14% inflation, the government has very limited room to offer meaningful concessions without undermining the fiscal consolidation that multilateral creditors require.

Subscribe to Latinsight publications for free and access a EU-Mercosur Business Opportunity Guide

Morales' enduring shadow over Bolivian politics

The purely economic reading of the crisis understates the role of organised political disruption. Paz has accused Morales of orchestrating the unrestto destabilise his administration. The march of Morales supporters that reached La Paz on May 18, coordinated over seven days from a starting point 180km away, was not a spontaneous mobilisation. Morales directed the march from his basein Bolivia's remote tropics, where he has been evading an arrest warrant for over a year and a half. The MAS candidate won just 3% of the presidential vote in October 2025, but the party retains significant organisational capacity in rural areas and among mining cooperatives — structures that were built over two decades and do not dissolve with an electoral defeat.

Former president Evo Morales still has a major influence on Bolivia’s politics. REUTERS

Morales' supporters are also motivated by a more immediate concern: the possibility that the government may move to arrest him in the coming days, which would transform a political protest into a direct confrontation over his personal fate. Eight Latin American governments released a joint statement rejecting destabilisation of Bolivia's democratic order, and the US State Department issued its support for Paz on Sunday. This sends a clear geopolitical signal that Washington's backing for Paz's reform programme remains firm.

🔎 Sectoral and investment outlook

The operational impact is immediate for companies with supply chain exposure in Bolivia. Road blockades have already disrupted gold cooperative miningand are rippling through trucking, agriculture and food distribution.

The arrest warrant against the COB's leader adds a new variable: if the labour union escalates its response, the already fragile partial agreements reached with miners and teachers could collapse, broadening the disruption further.

For the medium term, the investment case in Bolivia rests on two variables: the political survival of the Paz government and the pace of reform in the hydrocarbons and critical minerals sectors. Bolivia holds substantial lithium reserves, and the Paz government has signalled openness to foreign investment in extraction — but legislative instability and the ongoing social crisis make any timeline commitment unreliable.

The government's survival is not in immediate doubt as regional and US support is explicit and the military has shown no signs of defection. However, its capacity to legislate structural reforms while managing active social conflict is severely constrained. The next critical variable is whether the public prosecutor's move against the COB leader is enforced. If it is, the confrontation between the government and organised labour enters a qualitatively different phase — one that historical precedent in Bolivia suggests is very difficult to contain.