Codelco at a Crossroads

Chile’s copper sector contributes about 14% to Chile’s GDP and 58% of the country’s exports. Often regarded as an example of state-led company and public-private cooperation, Codelco is currently facing a steep production decline while the need for investment — in new projects, innovation and clean energy — seems more and more urgent. I analyze those challenges in this editio of The Chile Brief.

Chile’s giant state copper company is facing various key challenges.

Chile’s state copper giant is navigating one of the most turbulent periods in its recent history — and one of the most consequential for global copper supply. A production scandal, a leadership overhaul, a $24 billion debt pile, and a structural decline in output are arriving simultaneously, against a backdrop of elevated copper prices that should have been a windfall. The contrast is striking.

Leadership change

Bernardo Fontaine took over as chairman of Codelco’s board on May 27, replacing Máximo Pacheco. The appointment drew immediate scrutiny: Fontaine, an economist and former constitutional convention member, has no direct mining experience. The government framed the other new board appointments as complementary, making clear the mandate is institutional recovery rather than sector expertise.

The executive suite followed within days. On June 3, CEO Rubén Alvarado resigned, and the board named Jorge Gómez — former CEO of Collahuasi for 14 years, one of the most respected figures in Chilean copper mining — as his successor, effective July 13. His arrival from the private sector signals the direction Fontaine intends to take.

Fontaine’s own summary of the challenge is blunt:“Codelco is running with a lead backpack. We need to lighten it.”

The numbers behind the crisis

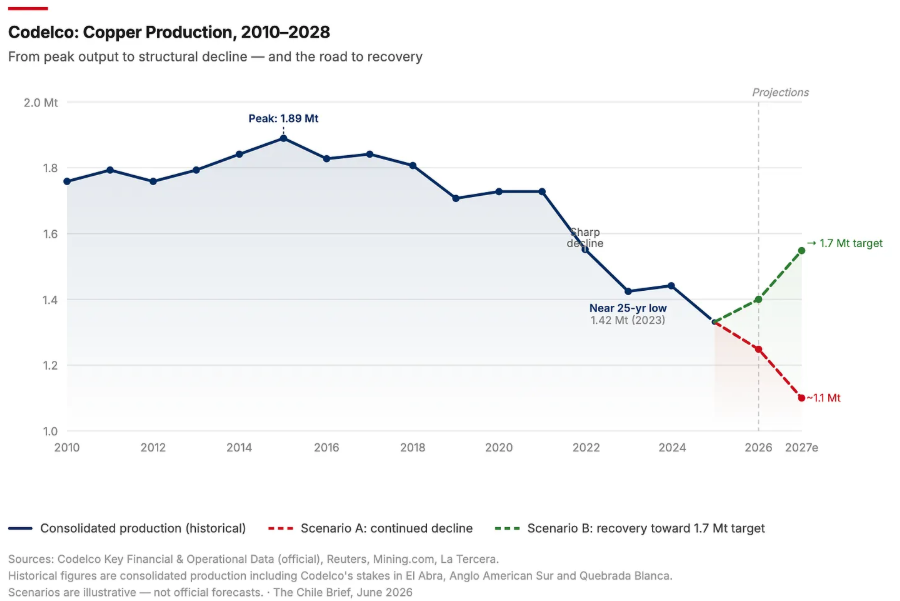

Codelco produced 272,000 tonnes of refined copper in Q1 2026, down 8% from Q1 2025 and well below the company’s long-run quarterly average of around 362,000 tonnes. Production has fallen from approximately 1.7 million tonnes annually to around 1.3-1.4 million tonnes — a structural decline that persisted through the largest investment cycle in the company’s history.

The cost picture is equally difficult. Direct production costs rose from 133 to 208.6 cents per pound between 2021 and 2025. Total debt now stands at $24 billion, having grown by $7.4 billion in four years despite $17 billion invested in structural projects over the same period.

The decline in production is mainly explained by the aging of super-pits. Codelco operates some of the oldest mines in the world in which copper concentration has decreased significantly, meaning the company must mine, process, and mill more rock to yield the exact same amount of finished copper as before. Old mines are also prone to more temporary shutdowns wether because of maintenance or accidents. Meanwhile, several major investments in new mines have been delayed[…]